It seems everyone, including myself, is expecting a deeper pullback in stocks. Usually, that means the opposite will happen, but sometimes the crowd is right. It's plenty overdue and there's a lot of good reasons like seasonality, the China issues, Fed tapering, a huge jobs miss in either direction Oct 8th, mean reversion, Fib retracement etc.. If it happens, I'm thinking it will be a dramatic shaking of the leverage tree on the order of about 20% to ES 3640, which is the 38% retracement of the rally off the March lows, and then a V reversal into year end.

It certainly could fall apart Sunday night, gap down and go, but with stocks you always have to ask yourself: what is the nastiest thing that could happen? And that would be first a move up above the consolidation over the 50-day to lure in FOMO longs and shake out the shorts into the Fed on Wednesday, then a nasty reversal that sets off the down move and closes the week below where we are now. It should be noted this could be wishful thinking because I'm currently flat equities hoping for a big down move to buy for a long-term hold. If for some reason stocks hold up this week, it's probably cancel crash, which would suck because I don't know how anyone buys at this level.

Daily ES.

Weekly ES.

Weekly Bonds. Will it be a risk parity meltdown across the board if taper is announced? Looks pretty head and shouldery in bond land. The tricky part is if stocks meltdown, bonds could catch a bid, so I'd rather wait on this myself because if the risk parity meltdown happens, it will create a great opportunity to put it on since bonds have no chance of sustaining downside beyond the long-term trend line.

Weekly Notes are looking like they want to go lower.

TNX. From yield perspective, it looks on the verge of a breakout. 1.429 is the level.

Weekly Dollar. If this breaks out and closes the week strong, it might test the long-term downtrend line. You can't deny everything is setting up for tightening, and this seems like the week it's waiting for. What do you say, Fed? Gotta pull the bandaid sometime.

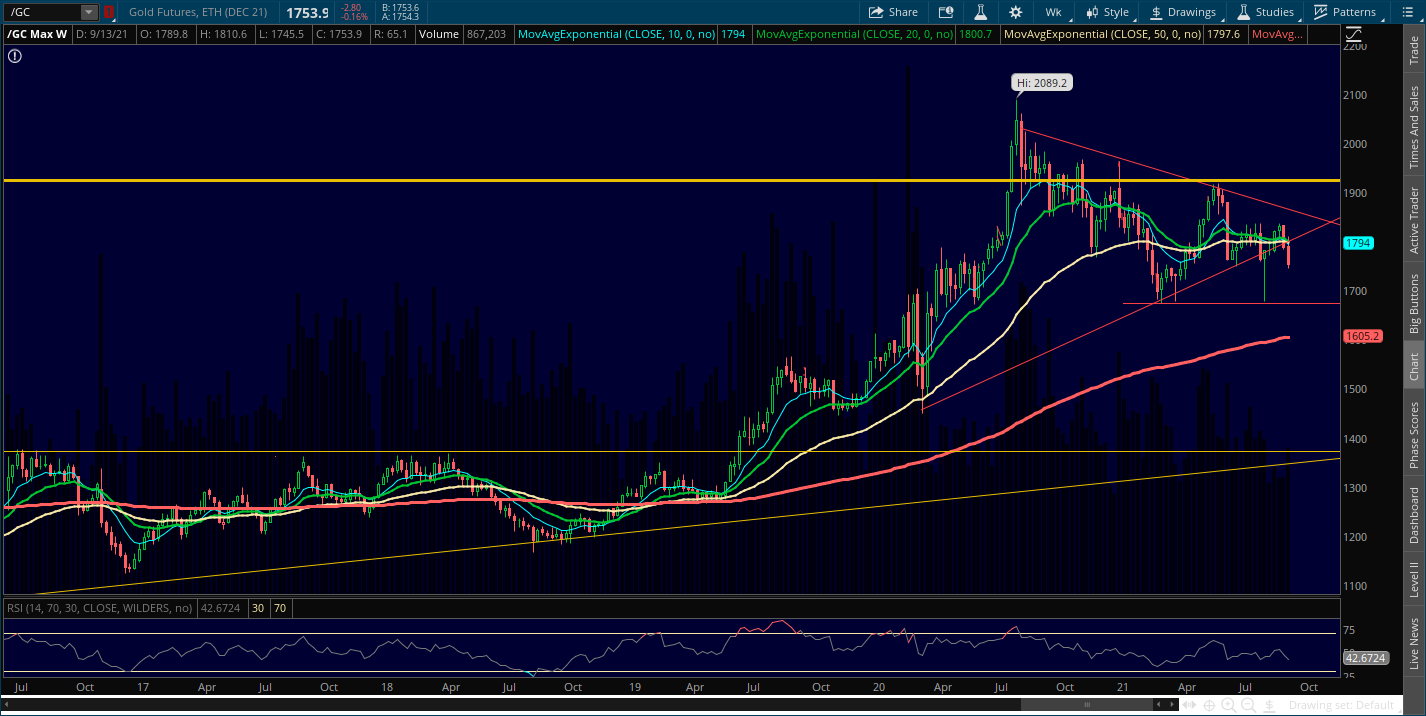

Weekly Gold. If the dollar jumps, gold likely dumps. Triple bottoms usually don't last long.

Weekly silver is looking nasty. I've been thinking for awhile if silver comes all the way to backtest the breakout of the $18/19 level it's a buy, but now that it might actually happen I'm second guessing myself because the metals suffer from so much supply from hedging, and I'd rather buy tech or crypto. We all know the Fed will never be able to normalize, so maybe silver and gold come down and make a new base to jump from in anticipation of the next time the Fed is forced to capitulate.

So here's the thing. I've forced myself to transform into an equity bull. And since I no longer put in the necessary screen time for short-term trading, I sent away for the PermaBull kit. It comes with a Tom Lee poster and Jim Cramer mug. And a t-shirt that says: I'm with them now (which could be a really bad sign, btw). I've always loved tech, and while it's overdue for a whacking in the short-term, I look at the world and think it's all going to follow our lead and adopt developed world technology, meaning, globalization has expanded the TAM for tech in ways that aren't even close to saturated. And that's not even counting new tech. As far as I'm concerned the internet bull market from the 90s is still the "general conditions" of the world. It's still evolving and expanding and penetrating markets. It popped in 2000 from overzealous buying, popped in 2008 from housing shenanigans, drawdowns in 2018's volmagedon, Covid in 2020, but it's still the same bull market in tech.

It's easy to fall into too much cynicism or focus too much on the end game problems caused by fiscal and monetary interventionism, but there's so much room for tech to penetrate developing worlds in the meantime, so I'm down with Cathie Wood and Elon Musk. She's onto all the great new tech themes, and I think Elon and crew are going to figure out FSD. I do think exponential trends need to be distinguished between physical and digital products, though, and between one company and its sector. Meaning, physical products are more challenging to scale exponentially due to production limitations, but digital products are not, so Tesla's valuation is very dependent on them solving FSD using only vision and neural nets because that allows them to license their digital intelligence to every car that's made in the future, including a robotaxi network. It's the digital tech that will scale exponentially. Without that, it's hard to imagine they can scale their physical cars enough to justify being valued so much more than the rest of the sector.

The other major limitation for Telsa is potential regulation, but a lot of that is optics. Every accident of FSD is going to blow up in the media while 10x that many human accidents go unreported, so it's largely a case of public perception. The future will look back and show an exponential trend of electric vehicles as a sector, but any single manufacturer within that sector is still limited by their production capacity.

Cathie Wood takes a lot of criticism, but most of that is unfair. She's investing in hyper growth companies, so the present day numbers are irrelevant. She's literally the definition of "skating to where the puck is going." Some people just overvalue the present and undervalue the future. Michael Burry might be right for about a month, but then he's gonna get smoked. It's kinda like people who focus on Ethereum's present day network numbers and don't see how superior Cardano is in its design, so they can't project into the future and see how they'll surpass Ethereum in every metric.

I must have spent well over 100 hours studying Cardano. There's not even a close second. They have over 100 peer-reviewed white papers about their design solutions. They've solved staking without custody or slashing. They've solved how to keep stake pools from centralizing. They've solved stable deterministic fees. They have a self-funding and voting mechanism, so in the future the stakeholders can find the optimal fee to incentivize validating, but not so high that it deters user growth. They're making it interoperable with other chains, so developers from Ethereum can easily migrate, or be on both. They're going to broaden the coding languages to those used by the majority of developers in the world outside of crypto. The hydra rollout will make it nearly infinitely scalable. And many of the most intelligent people in this space don't get it yet. Cardano could make this easier with a video that contrasts the pros and cons of their design decisions against other cryptos, but they will flip Ethereum within 2 years, Bitcoin within 5 years, and Apple within 10 years. Hopefully, while they're all going UP. If you've come to another conclusion, I would suggest spending more time studying what they are doing.

This next pic is an example of a 24hr period of recent stats. Transaction volume: Cardano 14.9B, Ethereum 9.9B. Active addresses: Cardano 148k, Ethereum 540k. Fees: Cardano $14k, Ethereum $33M.

Here's a link to their design rationale material: Cardano

BTC Daily - probably needs to take out the recent low and fill out the triangle before going higher (if I'm right about the Bitcoin thesis being wrong, it could take a year or two for the other crypto ecosystems to develop enough for that to become obvious, so I hope in the meantime Bitcoin keeps trending up since the whole space still trades as one).

ADA Daily. I'm thinking ADA trades down to possibly double bottom around $2, but crypto is just as nasty as the ES, which means usually structure has to get penetrated to shake the tree before reversals happen. $2 would be ~50% retracement of the rally from $1, and Bitcoin $40k would be ~50% of the rally from $29k to $52k. Maybe the whole world goes risk off for a month.

Another interesting development are the social tokens and how they could change the nature of employment. When I've had time, I've noticed Raoul and the Real Vision crew do a great job staying on top of this constantly shifting landscape. Here's an interesting video on DAOs and social tokens: Realvision